FireBreak Insurance

Parametric wildfire coverage for homeowners in wildfire severity zones. Submit photos of home hardening and defensible space to qualify for supplemental coverage that home insurance policies don't cover.

Safer from Wildfires

Safer from Wildfires is an interagency partnership between the California Insurance Commissioner and the emergency response and readiness agencies in the California Governor's office to protect lives, homes, and businesses by reducing wildfire risk.

This “ground up” approach for wildfire resilience has three layers of protection to prevent wildfires from catching and spreading to other homes and businesses in the neighborhood.

- Protect the structure: Home hardening

- Protect the immediate surroundings: Defensible space

- Protect the community: Firewise programs

Some home insurance companies give discounts based on layers 1 and 2, also known as Parcel Mitigation. Firebreak Insurance gives fast-payout supplemental coverage for expenses these traditional policies don't cover based on photo verification of layers 1 and 2.

1. Protect the structure: Home hardening

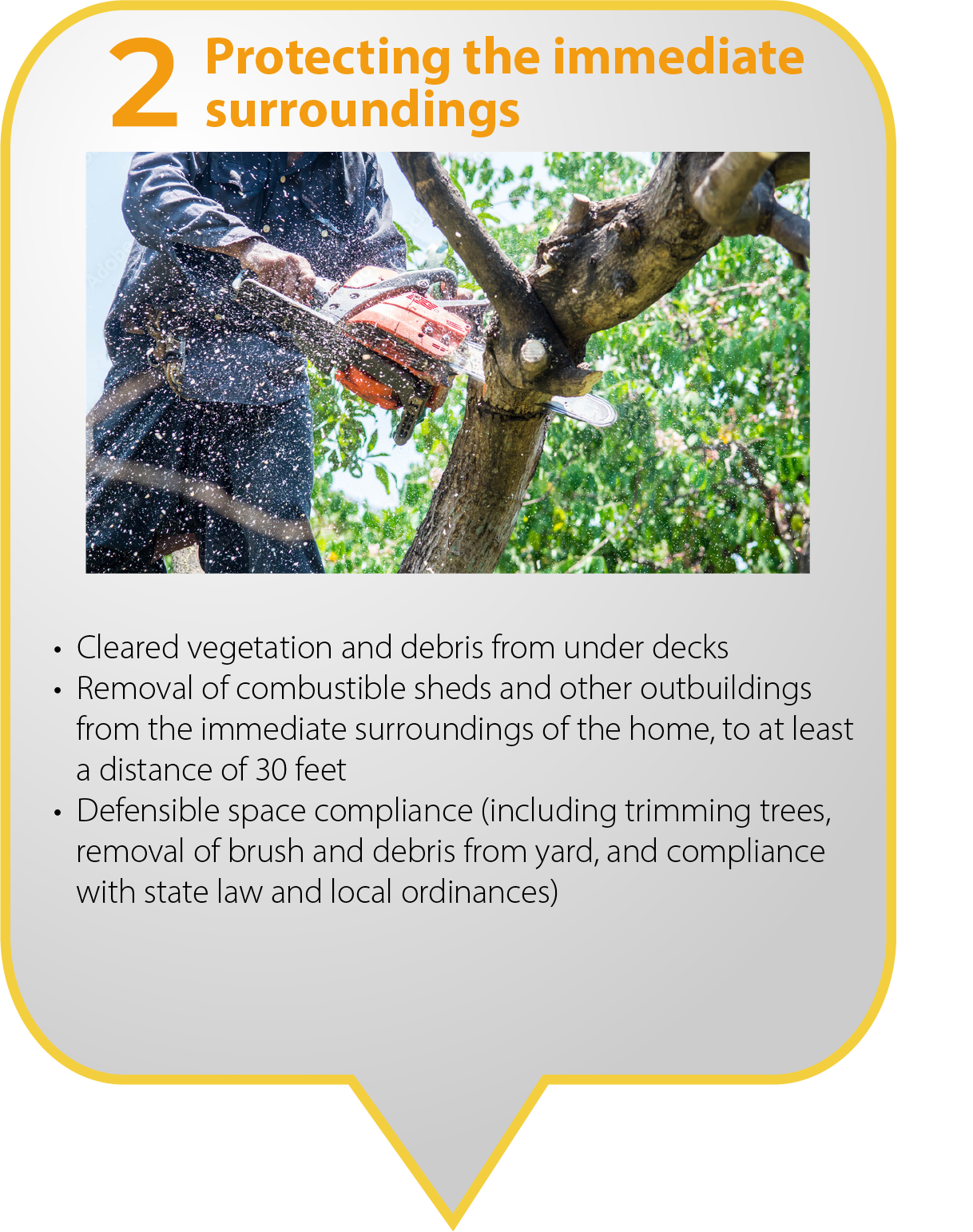

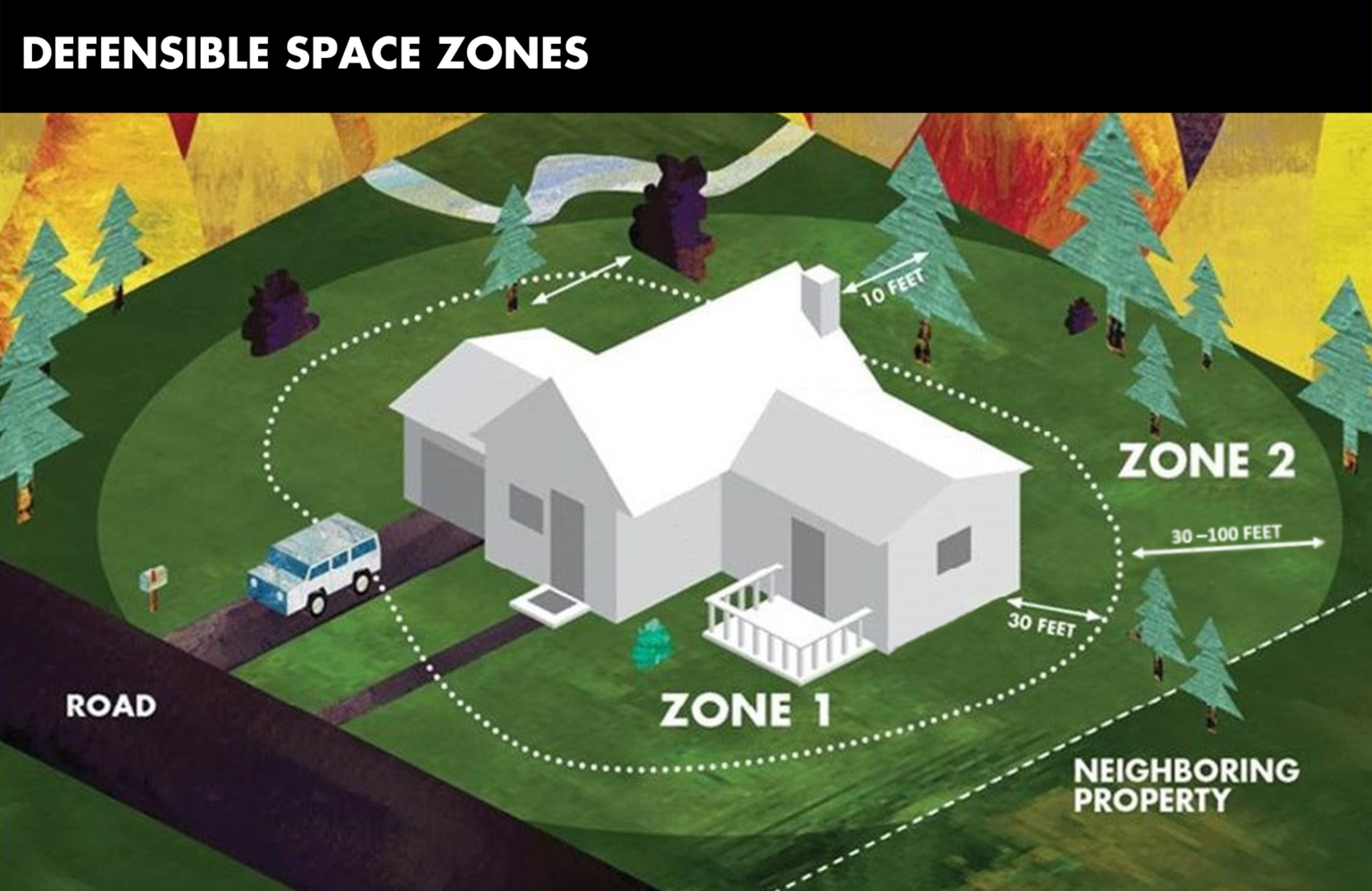

2. Protect the immediate surroundings: Defensible space

- Buffer zone between your home and the surrounding grass, trees and shrubs

- Slows or stops the spread of wildfire

- Protects your home from catching fire from embers, flame or radiant heat

- Gives firefighters a safe area to work in to defend your home.

How FireBreak Insurance works

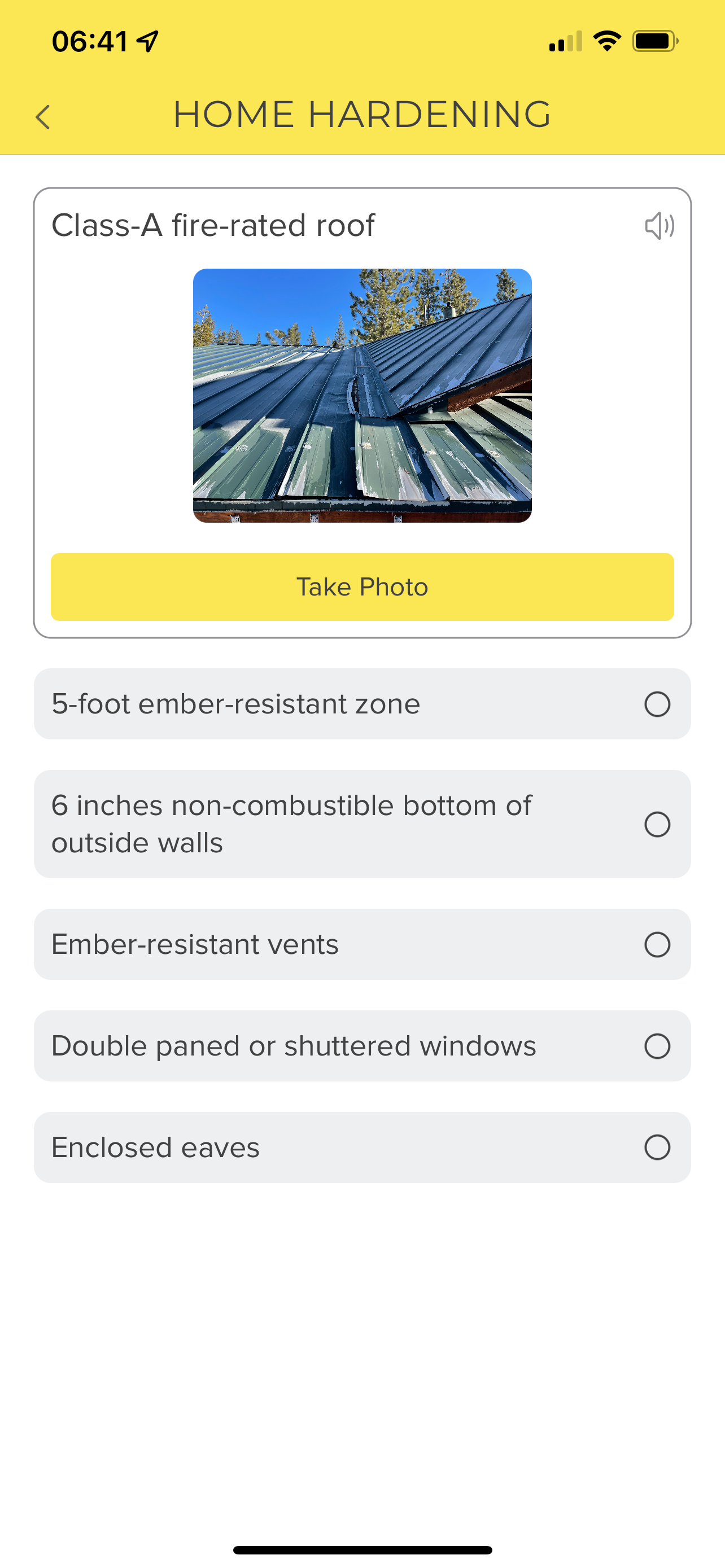

FireBreak Insurance verifies home hardening and defensible space using photos taken by the applicant using the FireBreak Insurance mobile phone app. In the aftermath of a wildfire evacuation and photo-verified fire damage, it pays out in days.

Homeowner application

• Defend your home from the next wildfire by following "Safer from Wildfires".

• Qualify for discounts on home insurance from participating carriers.

• Apply for FireBreak supplemental wildfire insurance by uploading walkthrough photos of your home hardening and defensible space on the FireBreak app.

• Pay premium with ACH

Homeowner claim

• After evacuation order

• Upload photos of fire damage to home on Firebreak Insurance mobile phone app.

• Get payout to same ACH account in days after claim.

Actuaries

• Base premium of 2% of payout

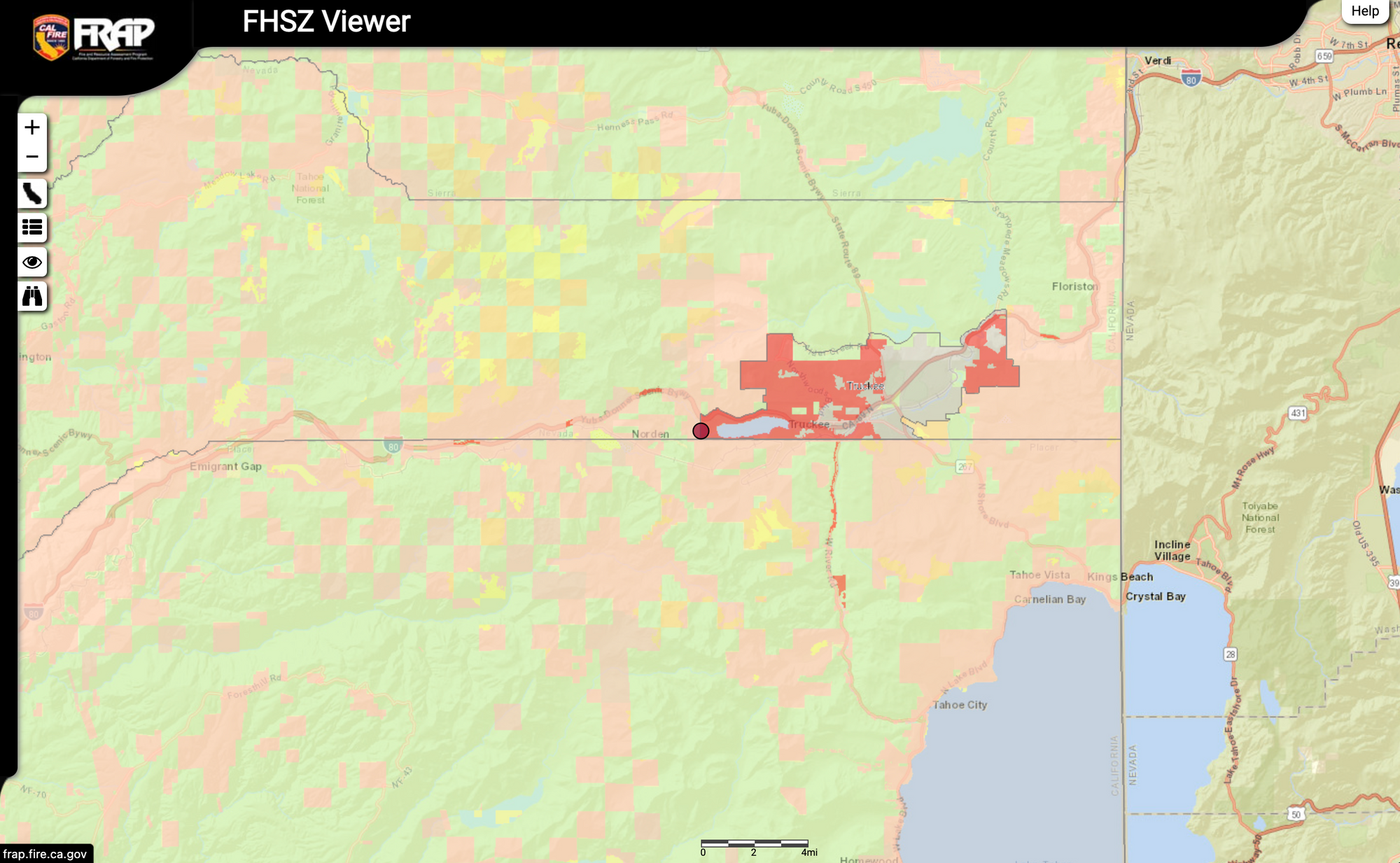

• Parameter 1: CalFire California Fire Hazard Severity Zone Maps by address

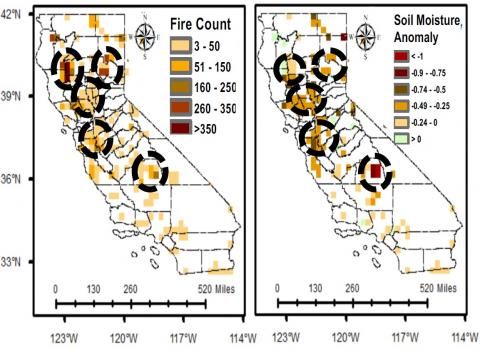

• Parameter 2: NASA Soil Moisture Active Passive (SMAP) satellite data by address. NASA has found a strong correlation between the timing and location of low soil moisture conditions and an increase in fires.

• Parameter 3: Betterview defensible space score including RedZone scores to distance to nearest fire station and hydrant.

An additional adverse selection mechanic recognized by the California Department of Insurance in the FireWise programs is that clusters of homes that have proactively pepared for fire compound the protection and break the chain of combustion.

Policy Limits and Premiums

Home values in places such as Lake Tahoe and Napa Valley have seen 2x or more spikes as tech workers and billionaires have moved to beautiful but unworkable places. The accelerated gentrification of resort towns has pushed up rents and lower paid construction contractors and laborers. Along with inflation, construction and equivalent home replacement costs have rocketed. A roof job in May 2022 on a small 1,500 sq ft. Truckee home now quotes at $50k with labor charging $175/hr.

Coupled with a retraction reinsurers in the regions, there is less capacity to meet the increasing cost of replacement so less policies and more cancellations. Vineyards in Napa and mountain homes feel the same pinch and are underinsured or are left to self-insure.

Homeowners are spending $10k’s on defensible space and home hardening. These are good risks. But given the lack of capacity remain underinsured. FireBreak insurance aims to cover the gap in home replacement value. In March 2022, Truckee home prices were up 41.8% compared to last year, selling for a median price of $1.4M.

Rates

Homes without defensible space would pay 2x the 2% premium base rate and those with defensible space 0.5x the base. In addition properties with 75% more defensible space in zone 2 (30-100 feet from the building) that are 1.6x more likely to survive a wildfire undamaged would pay 1/1.6th or 0.625% in premium.

Example Premium

So a typical FireBreak Insurance policy for a Truckee home with 75% zone 3 defensible might expect to cover the medial increase of $400,000 and earn a premium as low as $2,500. Without defensible space the premium would be as high as $16,000. A homeowner looking to fully insure a $1,400,000 home with 75% zone 3 defensible space would pay $8,750. Or without defensible space $56,000.

Alternative Fixed Pricing

A pricing model being explored is to fix the premium price as tokens of $1,000 that pay out depending on the risk exposure of the property. A homeowner with 75% zone 3 defensible space could purchase $1000 bets that pay out $160,000. Without defensible space the payout would be $25,000.

Underwriters

Pre-inspect homes remotely using insured-uploaded walkthrough photos of compliance with "Safer From Wildfires" California Department of Insurance recommendations.

• New Quotes

• Renewal

Claims adjustors

When processing wildfire damage claims

• Monitor homes for evacuation orders from CalFire Incidents index

• Contact insured and verify if home was damaged in the fire using insured-uploaded photos of roof

• Flat-fee payout via ACH account paid in to keep margins low